Flooding is a major issue in the UK, with around one in six properties at risk of flooding from coastal, river and surface water(1). It is generally caused by extreme weather events, for example heavy rainfall can damage inland towns and stormy conditions can flood the coastline(2). In the past few years, flooding has made the headlines as a key issue affecting towns across the UK. The 2014 floods came alongside the wettest winter since 1766(3). In 2015, Storms Desmond, Eva and Frank battered the UK, leading to 16,000 homes flooded(4).

The UK may not suffer the tornadoes and wildfires seen in other parts of the world, though a combination of factors has left it particularly susceptible to flooding. Houses continue to be built on flood plains due to the picturesque locations of coastal towns, and the fact that the land is relatively cheap for developers to buy(5). The many fields and open spaces in the UK used to help manage flooding as water would be absorbed into the ground. With the rise of tarmacked retail parks and people opting for patios rather than lawns, the natural flood management system is under strain as the water has nowhere to drain to(6).

Due to climate change, flooding is expected to become a bigger issue in the years ahead. Recent research by Newcastle University found that 85% of UK cities with a river are expected to see more frequent flooding by 2100(7). Today, the issue costs the UK around £1.2 billion each year, with estimated costs between £1.6 and £6.8 billion by the 2050s(8).

Creation of Flood Re

Flood Re was created as a response to this, with the Government and insurance industry deciding that a collaborative solution was needed to address these issues. Householders living in high-flood risk areas faced the prospect of significant increases in the cost of insuring their homes.

The variability in flood events made the situation worse. In 2010, there were only around 6000 flood-related household insurance claims, whereas in 2007, there were almost 70,000(9). The industry has to balance competitive rates for customers with the high cost of paying out flood claims. However, this is of little comfort to those who live in some of our most beautiful coastal towns, or who wanted to continue living in their childhood home. For these people, flood risk means they either had to pay very high premiums or accept large excesses on a future claim.

The system in place before Flood Re was based on the Flood Insurance Statement of Principles, which committed insurers to providing flood insurance to existing customers and committed the Government to invest in managing flood risk(10). These principles were introduced in 2000 as a temporary solution to the problem. However, it restricted consumer choice as insurers were only committed to their existing customers. New insurers could decide to whom they offered flood insurance, and the statement made no reference to ensuring the insurance was affordable. It was later decided by both the insurance industry and the Government that this was not sustainable.

The Government worked with the insurance industry to create Flood Re. The aim was to offer a scheme that gave affordable flood cover to those at highest risk of flooding and increase availability and choice of insurance companies for consumers. It was also hoped this would act as a transitional measure with the aim of reaching affordable risk-reflective pricing within 25 years. Furthermore, the scheme was intended to help create a level playing field for new entrants and existing insurers in the UK home insurance market(11).

Discussions between the industry and Government took place during 2014 and 2015, before the scheme was formally launched in April 2016 under the Water Act 2014. The insurance industry paid over £20m for the initial setup costs of Flood Re(12). Parliament agreed that it would function as an operationally independent organisation, making best use of the insurance industry’s expertise. The statutory levy placed on all home insurers required that Flood Re would also be directly accountable to Parliament.

Flood Re was designed with a fixed life span. Its primary focus is on helping customers who are currently facing flood risks. In the long-term it aims to encouraging other parties to improve flood management. A first transition plan was published in February 2016, outlining the direction that Flood Re would like to see to enable affordable insurance for high flood risk households in the open market in the future(13).

How Flood Re works

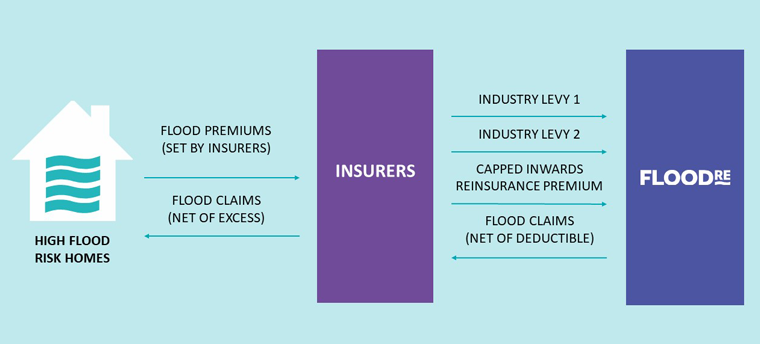

Flood Re allows insurers to pass the flood risk element of home insurance policies bought by customers to Flood Re(14). It receives £180m from a Levy on home insurers, raised in proportion to each insurer’s market share.

The Levy funds an outwards reinsurance programme to protect the Scheme up to a £2.1bn maximum liability limit. Secondly, it enables Flood Re to offer premiums below the rates insurers would normally charge on properties at high risk of flooding (although the premium is still sufficiently high to ensure that insurers only cede policies of high-risk properties to Flood Re). Thirdly, it funds the cost of any claims. This ensures that the industry retains a large portion of household flood risk that can affordably and profitably be covered in the open market. If the £180m levy is not enough for Flood Re to meet its capital requirement, then it can issue a compulsory call for additional funding from the industry through Levy 2(15).

When a householder who has taken out a home insurance policy backed by Flood Re makes a claim due to flooding, they continue to deal directly with their insurance provider. The insurer is then reimbursed by Flood Re for the cost of the claim. In return for taking the flood risk element of home insurance from an insurer, Flood Re charges the insurer a premium based on the property’s council tax band, called the “Inwards Reinsurance Premium”.

Flood Re is focused on domestic households rather than businesses as it was found that there was no evidence of a systemic failure in the business insurance market, nor was it deemed appropriate that individual householders should be placed in a market that cross-subsidises commercial business activity. It was also decided that it would not cover homes built after 2009, as this would risk incentivising inappropriate development in areas at risk of flooding.

The infographic below shows how this works.

Figure 1. Basic Principles of Flood Re (16)

How Flood Re fared in its first year

Flood Re was launched in April 2016. From the start the scheme enabled insurers to offer competitive premiums and lower excesses. 127,000 homes across the UK benefitted from the Scheme in its first year.

Flood Re wanted to raise awareness of the scheme to ensure that all eligible householders were benefitting. In September 2016, a Flood Re team began cycling from Land’s End to John O’Groats – a gruelling 1,120-mile journey from the UK’s most southwest to most north-easterly point in just a week and a half. The team stopped in areas susceptible to flooding to raise awareness of the scheme and to update local media outlets on the improved support available for householders(17).

Figure 2. The Flood Re cycling team in John O'Groats (Scotland), after completing their 1.800 Km journey across Great Britain.

Results today

Flood Re is successfully working towards meeting its objectives and has received support from the media and politicians across all parties.

After 18 months, Flood Re has backed 142,000 policies(18). Insurers also appear to be retaining more policies than they originally expected, increasing the level of cover for those in flood-risk areas beyond the cover provided by Flood Re.

Affordability for households has also improved; four out of five householders who have made previous flood claims have seen a reduction in the price of policies available to them by more than 50%.

The scheme is meeting its objective to increase the availability and choice for consumers. Before the introduction of Flood Re, only 9% of householders who had made prior flood claims could get quotes from two or more insurers, with 0% being able to get quotes from five or more. By January 2018, availability had improved so that 100% of those surveyed could get quotes from five or more insurers(19) – and 74% of those with flood claims being able to choose from at least 10 insurers.

Flood Re is also ensuring that there is a level playing field for new entrants into the UK home insurance market, with the £180m levy being raised proportional to their market share of business written(20).

Flood Re has secured widespread support from across the insurance industry, with Flood Re backed policies available through more than 60 insurance brands, representing 90% of the home insurance market(21).

It has also secured a strong financial position with substantial reserves in year one. The scheme’s solvency capital ratio was 237% as of March 2017, and it has received a preliminary rating of an A- (stable) outlook by Standard and Poor’s.

What's next for Flood Re

Flood Re will cease to operate in 2039, when it is hoped that the system will no longer be necessary. The end goal is a home insurance market with affordable 'risk-reflective’ pricing - where household flood insurance is affordable and widely available. The majority of actions that will be needed to reduce the cost of home insurance are not under the direct influence of Flood Re. For example, the scheme has no power to control flood defence investment, building regulations, household behaviour or climate change policy. However, Flood Re will play an important part in encouraging a wider effort to tackle flooding. Therefore, Flood Re will act as a convenor, working with all stakeholders to ensure that the UK takes concrete action so that in a post-2039 world without Flood Re, households in flood-prone parts of the UK can still access the home insurance products that the Scheme’s operation has made possible today. Preliminary ideas for transitioning to risk-reflective pricing were outlined in the first Transition Plan in February 2016, with an updated document being published later this year(22).

As part of preparing for its Transition, Flood Re is commissioning research into how to best move towards affordable risk-reflective pricing. Flood Re is considering how to incentivise households to implement property level flood resilience and resistance (“PFR”) measures. This refers to a variety of products that can protect a property against flooding, including anti-flood doors, anti-flood airbrick replacements and non-return valves. Flood Re commissioned a report from the University of the West of England exploring the financial viability of PFR measures, including both post-flood repair and proactive resilience intervention. This research has yet to be completed, but published interim conclusions suggest that PFR measures are beneficial and play an important role in flood risk management.

A second report with the Social Market Foundation (SMF) looked at the options for incentivising PFR uptake(23). One policy that the report assessed was 'three strikes and you’re out’, whereby a household would be prohibited from having their policy ceded to Flood Re after the third time they were flooded if they did not take up PFR. The SMF report rejected this approach because it found that this would only have a marginal effect on PFR take-up, and it would ultimately deviate away from Flood Re’s objective of increasing the availability of affordable home insurance. Another policy option explored was a positive approach of rewarding those who implement PFR measures with lower premiums. Flood Re believes this has potential because it has precedents in other areas of home insurance - for example, with the voluntary installation of smoke detectors and mortice locks.

Flood Re therefore wants to raise awareness of flooding risks to householders to encourage them to take resilience precautions. One powerful way it did this was by launching a nationwide competition to find the country’s Local Flood Heroes. Supported by radio advertising, local newspaper coverage, MPs representing flood risk communities and social media activity, the campaign attracted nominations from every part of the UK. The competition culminated in an awards ceremony in the House of Parliament hosted by Floods Minister, Rt Hon Thérèse Coffey MP. Flood Re, in partnership with the insurers Covea and NFU Mutual offered a £10,000 prize for the winner to be contributed towards flood defences in their local area. After an exhaustive process, fierce competition and with so many worthwhile nominations the ultimate winner was Geraldine Brown. She was recognised by a judging panel for coming to the aid of her community at their time of greatest need during severe flooding. She helped set up an emergency contact centre and used a local church as a flood refuge in her village of Yalding in Kent(24).

Figure 3. From left to right, Rt HonThérèse Coffey, Parliamentary Under Secretary of State at the Department for Environment, Food and Rural Affairs; Geraldine Brown, Local Flood Hero award winner and Andy Bord, CEO of Flood Re.

In its two-year lifespan, Flood Re has benefitted thousands of householders who face a risk of flooding. It is meeting its core objectives to make available a wide choice of affordable flood cover and to work prepare for a transitional to affordable risk-reflective pricing within 25 years.

In March 2018, Flood Re announced that it will freeze the premiums it charges to insurers for ceding polices, rather than increase them in line with Consumer Prices Index. Flood Re anticipates this freeze will ultimately benefit consumers.

In the years ahead, Flood Re will continue to optimise the Scheme to benefit as many householders as possible and to contribute to a better understanding of flood risk management in the UK.

BBC News (2016) 'Storms Desmond and Eva flooded 16,000 homes in England’ (5 January 2016), BBC News [online]. Available at: http://www.bbc.co.uk/news/uk-35235502 (Accessed 27 February 2018).

Due to climate change, flooding is expected to become a bigger issue in the years ahead. Recent research by Newcastle University found that 85% of UK cities with a river are expected to see more frequent flooding by 2100.

Today, the issue costs the UK around £1.2 billion each year, with estimated costs between £1.6 and £6.8 billion by the 2050s.